CONVENTIONAL

Conventional loans are one of the most popular mortgage options for homebuyers. These loans are not backed by the government, offering flexibility with competitive interest rates and terms. Conventional loans are ideal for buyers with good credit and stable income, and they typically close faster than government-backed loans. Whether you're purchasing your first home or refinancing, our team can help you navigate the process and find the best solution for your needs.

VA

VA loans are a fantastic benefit for U.S. veterans, active-duty military, and eligible spouses. These loans offer competitive interest rates, require no down payment, and do not require private mortgage insurance (PMI). VA loans typically close faster than other government-backed loans, making the home-buying process more efficient. If you qualify, a VA loan could be the perfect choice for achieving homeownership with ease and minimal upfront costs.

FHA

FHA loans are government-backed mortgages designed to help buyers with lower credit scores or smaller down payments. With a down payment as low as 3.5%, they make homeownership more accessible. FHA loans often come with competitive interest rates, but they may require mortgage insurance. They also tend to close faster than some other government-backed loans. Whether you're a first-time homebuyer or looking to refinance, our team can guide you through the process and help you secure the best deal.

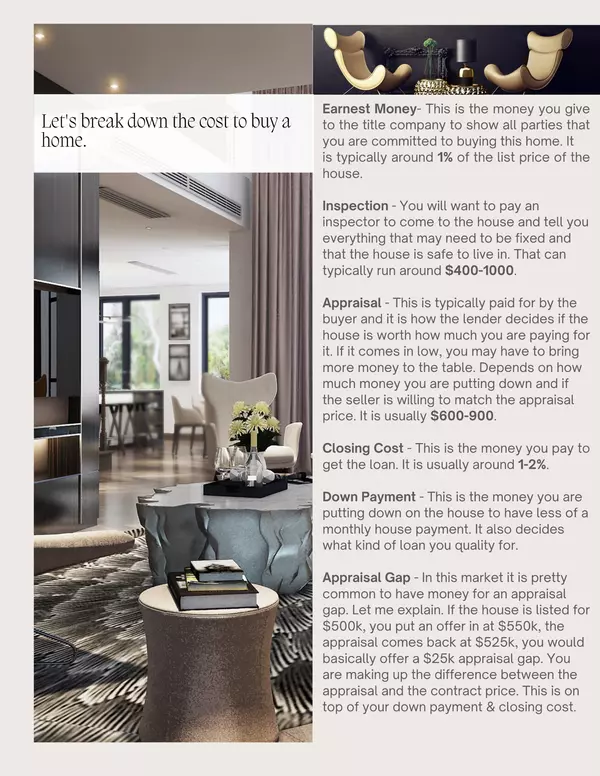

EARNEST MONEY

Earnest money is a deposit you provide to the title company to demonstrate your commitment to purchasing the home. This shows the seller and all involved parties that you’re serious about the transaction. Typically, the earnest money is around 1% of the home's listing price.

INSPECTION

It's important to hire a professional inspector to thoroughly assess the property. They will identify any potential issues that may need repair and ensure the home is safe to live in. This inspection is a crucial step in understanding the true condition of the house. The cost typically ranges from $400 to $1,000, depending on the size and complexity of the property.

APPRAISAL

The appraisal fee is typically paid by the buyer, and it helps the lender determine if the home is worth the price you're paying. If the appraisal comes in lower than the agreed-upon purchase price, you may need to bring additional funds to cover the difference, depending on your down payment and whether the seller is willing to adjust the price to match the appraisal. Appraisal fees usually range from $600 to $900.

DOWN PAYMENT

The down payment is the amount you contribute upfront toward the purchase of the home. A larger down payment can help reduce your monthly mortgage payments and may also influence the type of loan you qualify for. It plays a key role in determining your loan terms, interest rate, and overall affordability.

CLOSING COST

This is the fee you pay to secure the loan and cover the costs associated with processing your mortgage. Typically, it ranges from 1% to 2% of the loan amount, depending on the lender and the type of loan.

APPRAISAL GAP

In today’s market, it's becoming increasingly common to have funds set aside for an appraisal gap. Let me explain how this works: If a home is listed for $500K and you make an offer for $500K, but the appraisal comes back at $475K, you'd need to cover the $25K difference between the appraisal value and the agreed-upon purchase price. This is known as an appraisal gap. Keep in mind, this amount is in addition to your down payment and closing costs, so it’s important to factor it into your budget when making an offer.

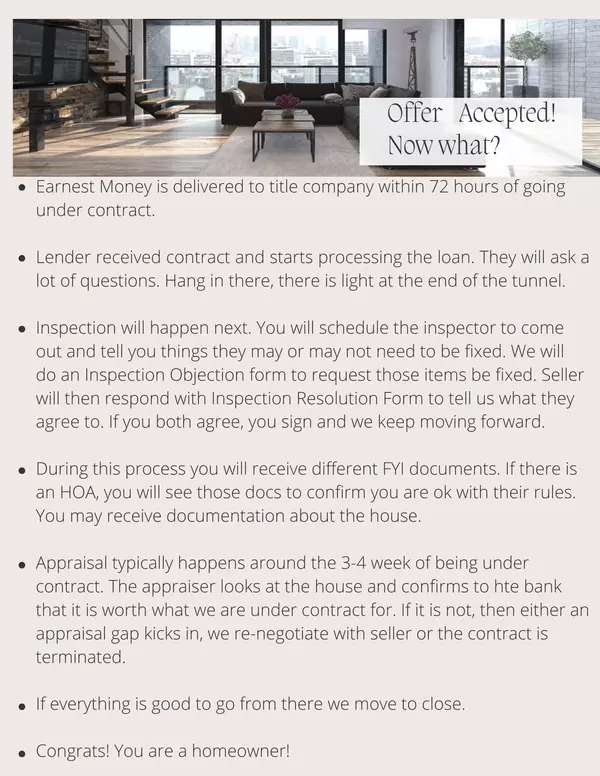

3. INSPECTION

You’ll schedule a home inspection, where the inspector will identify any issues that may need attention. If necessary, we’ll complete an Inspection Objection form to request repairs or concessions from the seller. The seller will then respond with an Inspection Resolution form, outlining what they agree to address. If both parties reach an agreement, you’ll sign, and we’ll continue moving forward with the process.

3. DOCUMENTS

Throughout this process, you’ll receive various informational documents. If the property is part of a homeowners association (HOA), you’ll review the HOA documents to ensure you’re comfortable with their rules and regulations. Additionally, you may receive other relevant documents about the property itself, providing important details for your review.

5. APPRAISAL

The appraisal typically takes place 3-4 weeks after going under contract. The appraiser evaluates the property to confirm its value aligns with the agreed-upon contract price. If the appraisal comes in lower than expected, you have a few options: an appraisal gap may come into play, we can renegotiate with the seller, or, in some cases, the contract may be terminated.

6. CLOSE

If everything checks out and all conditions are met, we’ll proceed to closing. At this stage, all paperwork will be finalized, funds will be transferred, and you’ll officially become the owner of your new home. We’ll guide you through the closing process to ensure everything goes smoothly and you're fully prepared for this exciting milestone.

Click on the links below