What Is a Seller Carry Loan and How Does It Work?

What Is a Seller Carry Loan and How Does It Work?

What Is a Seller Carry Loan and How Does It Work?

Imagine finding your dream home, only to hit a wall with traditional mortgage lenders. Maybe your credit isn’t perfect, or your income is tricky to document. Enter the seller carry loan—a creative solution that can unlock homeownership for buyers and open new opportunities for sellers.

What Exactly Is a Seller Carry Loan?

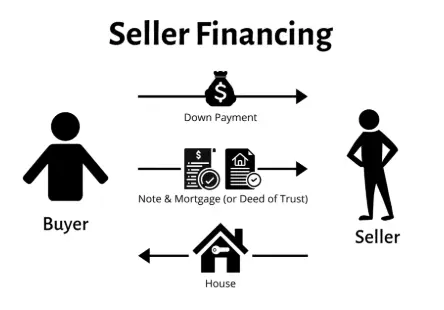

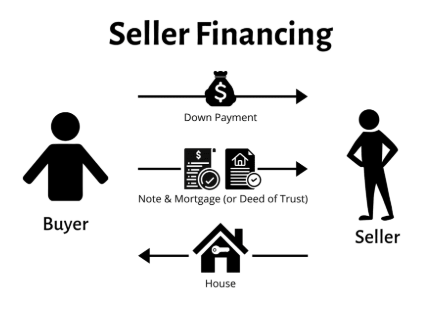

A seller carry loan, also known as seller financing or owner financing, flips the script on the typical home-buying process. Instead of a bank providing the loan, the seller steps in as the lender. The buyer and seller agree on the loan terms, and the buyer makes payments directly to the seller—usually with interest—over an agreed period.

How Does It Work?

Here’s the basic flow:

- The buyer and seller negotiate the price, down payment, interest rate, and repayment schedule.

- The buyer makes a down payment (often more flexible than traditional requirements).

- The seller draws up a promissory note outlining the loan terms.

- The buyer pays the seller monthly, just like a mortgage.

- Once the loan is paid off, the seller transfers the title to the buyer.

Why Choose Seller Financing?

- For buyers: It’s a lifeline for those who may not qualify for a conventional loan—think self-employed individuals, freelancers, or those with less-than-stellar credit.

- For sellers: It can attract a wider pool of buyers and provide a steady income stream, often at a higher interest rate than a savings account or other investments.

What Are the Risks?

- Sellers: There’s the risk of buyer default, so it’s crucial to vet buyers and have a solid contract in place.

- Buyers: Interest rates may be higher, and the repayment period might be shorter than a traditional mortgage.

Real-Life Example

Let’s say a seller wants $300,000 for their home. The buyer can’t get a bank loan, so the seller agrees to finance $250,000 at 6% interest over 10 years. The buyer puts down $50,000, then pays the seller each month until the balance is paid off. When the final payment is made, the buyer receives the home’s title—no banks involved!

Seller carry loans aren’t for everyone, but they can be a win-win with the right planning and protections. Always consult a real estate professional and attorney to make sure everyone’s interests are protected and the process goes smoothly.

Categories

Recent Posts